P2P News CW 08/2026: Afranga SaveSmart Starts New Fixed-Interest Product

Welcome to the latest P2P lending news. One of the most notable developments this week is the launch of Afranga SaveSmart, a new fixed-interest investment product offering monthly interest payouts to investors. With this move, Afranga expands its product lineup and aims to attract investors looking for predictable cash flow in the P2P lending space.

At the same time, several other platforms are making headlines. Rendity has officially announced the shutdown of its operations and has started the wind-down process for a platform that once served more than 38,000 investors and facilitated over €150 million in funding. EstateGuru continues to struggle with non-performing real estate loans, particularly in the German market, while InRento is seeing its first two projects come under pressure.

Meanwhile, FF Forest shared new insights in its first Q&A session, discussing topics such as CO₂ certificates, expansion plans, institutional investors, and potential interest rate reductions.

In this edition, we take a closer look at what these developments mean for investors — starting with the launch of Afranga SaveSmart.

Please note my disclaimer: I do not provide investment advice and I do not make any individual investment recommendations. This article reflects only my personal opinions and observations and is intended for informational purposes only. Investing in P2P loans and project financing involves risks, including the possibility of a total loss of your invested capital. Past performance is not a reliable indicator of future results. Links to investment platforms may be affiliate or promotional links (usually marked with *), meaning I may receive a commission if you sign up or invest through them. All content and ratings are created independently and are not influenced by any platform provider.

Table of Contents

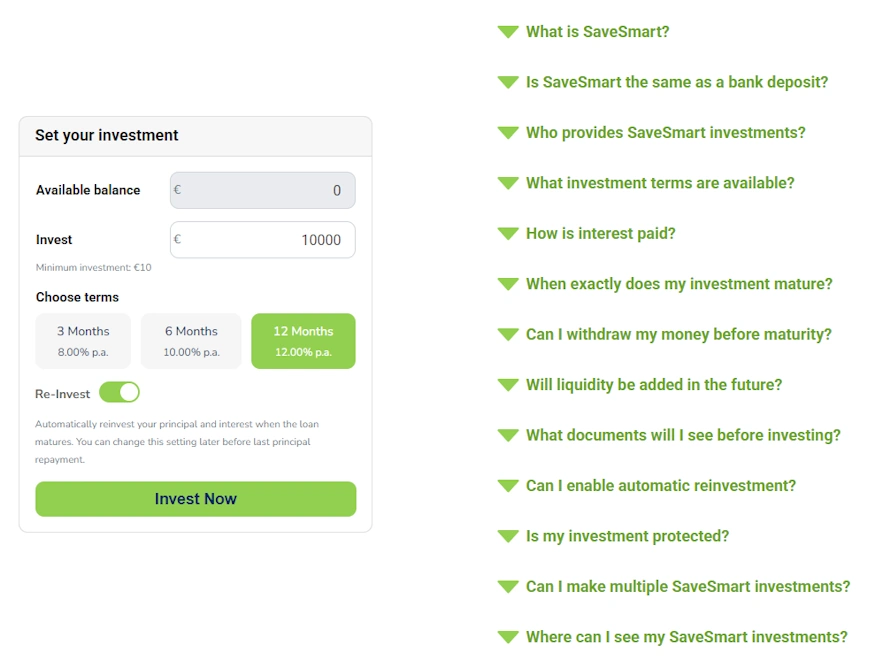

#1 Afranga SaveSmart launches with fixed investment terms

With Afranga SaveSmart, the platform Afranga has introduced a new fixed-interest investment product. The structure is simple:

- a fixed term,

- a clearly defined interest rate,

- monthly interest payments,

- and repayment of the invested capital at the end of the term.

At launch, the product is funded by the loan originator Stikcredit. Investors can currently choose between three different maturities:

- 3 months – 8% interest

- 6 months – 10% interest

- 12 months – 12% interest

Interest from Afranga SaveSmart is paid out monthly to the investor wallet, while the principal is repaid as a bullet payment at the end of the investment term. Early withdrawal is not possible. However, investors can activate automatic reinvestment, allowing the capital to be reinvested automatically at the interest rate available at that time.

From a legal perspective, Afranga SaveSmart remains a direct loan agreement between the investor and the loan originator under ECSP regulation. As with typical P2P investments, there is no deposit protection scheme.

With this launch, Afranga SaveSmart follows the broader industry trend toward “vault-style” investment products that provide predictable cash flows and a simplified user experience. By combining several maturities, investors can build a laddered structure that regularly frees up capital for reinvestment.

Similar concepts such as Monefit SmartSaver or Modena show how popular these structures have become among P2P investors. Overall, the concept behind Afranga SaveSmart makes sense — although the product name itself might not win any creativity awards.

#2 First InRento projects under pressure

InRento is now facing its first problematic projects. The investments “46 Lofts Kaunas” and “Liberty 72B Kaunas”, both issued by the same borrower, have reported payment delays.

According to InRento, the project developer is currently experiencing liquidity issues. A planned sale of a managed property in December 2025 was not finalized, which resulted in delayed interest payments to investors. Both projects are secured by a first-rank mortgage, and the loan-to-value (LTV) ratio is reportedly capped at 70% according to the platform.

The borrower is now attempting to stabilize the situation by selling additional properties and negotiating with a financial institution for refinancing. As stated in the loan agreement, penalty interest of 0.2% per day applies to overdue amounts.

If the situation cannot be resolved, enforcement measures could be initiated. This would mark the first time such recovery procedures might be required on InRento, making the outcome of this case particularly interesting for investors to watch.

#3 Rendity shuts down operations after years of problems

The Vienna-based real estate crowdfunding platform Rendity has now officially shut down its operations after years of negative press and poor investor reviews. No new projects had been offered since April 2024, and the platform is now entering the final wind-down phase.

According to the announcement, the platform will likely remain technically accessible until May 31, 2026, allowing investors to withdraw remaining balances.

In total, around 38,000 investors invested more than €150 million across 222 projects. However, less than half of this capital has been repaid so far. Many project issuers are currently facing delays, restructurings, or insolvency proceedings.

The investments on Rendity were structured as subordinated loans, meaning investors had a direct contractual relationship with the project company, not with the platform itself. Rendity therefore points to the issuers as responsible parties, a position that many investors see as highly problematic. As things stand, it is likely that millions of euros in investor funds could ultimately be lost.

The company’s 2024 financial statement highlights the difficult situation. After posting a €1.1 million profit in 2023, Rendity recorded a loss of nearly €1 million in 2024. Equity shrank to €709,000, and the German subsidiary has already been liquidated.

Investors are advised to check their bank details and withdraw any remaining balances. Several lawsuits are already underway, and the shutdown represents yet another setback for the already struggling real estate crowdfunding sector.

#4 EstateGuru continues to struggle with legacy defaults

After the shutdown of Rendity, many investors are inevitably turning their attention to the Estonian real estate platform EstateGuru, whose overall investor ratings are not much better. The platform is still dealing with a significant number of legacy defaults and has recently published another update on the recovery process for non-performing loans. The situation in Germany remains particularly challenging.

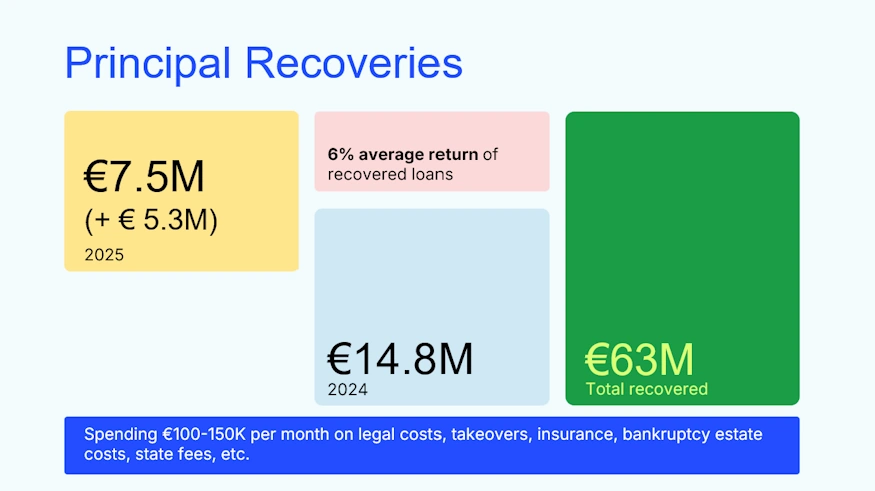

According to the latest portfolio overview, a large share of the defaulted loans originates from the German market. Out of roughly €108 million in defaulted loans, around €76 million are linked to German projects. Recoveries are progressing only slowly, as many cases are tied up in lengthy enforcement procedures, insolvency processes, or property liquidation sales.

So far, five projects have been recovered, albeit with substantial losses for investors. EstateGuru expects a similar number of recoveries in Germany during the first half of 2026.

The platform emphasizes that it is working intensively on restructuring loans and enforcing collateral. In Germany, this often involves foreclosure auctions, time-pressured property sales, and legal disputes, all of which take time and significantly reduce potential returns. The theoretical protection offered by mortgage-backed lending can look very different in practice when project developers run into financial trouble in a weak real estate market.

EstateGuru itself is also bearing considerable costs. According to the platform, it currently spends six figures per month to manage the recovery and legal processes for problematic loans.

That said, EstateGuru is unlikely to become another Rendity. Unlike the Austrian platform, EstateGuru continues to develop its business model and actively attract new investments, still raising millions of euros each month. As long as that continues, the platform itself is unlikely to face an immediate existential threat — although affected investors will still need to bring a lot of patience.

#5 First FF Forest Q&A provides insights into business model and strategy

FF Forest has published its first Q&A session, offering investors a closer look at the company’s business model, collateral structure, and future expansion plans. While the session was not held live, it still provided several clear statements on how the platform operates.

One of the main topics discussed was CO₂ certificates, which play a role in the long-term value creation of the forestry projects. According to the company, each certificate represents one ton of captured CO₂. After verification by the relevant authorities, the reforestation areas are registered with Verra, one of the major global carbon credit standards.

The first certificates are expected to be issued no later than five years after planting. However, the company also mentioned that forward sales with discounts or long-term offtake agreements of up to 20 years are possible.

Another key topic was Timbro, the company behind the projects. The core business model focuses on acquiring forest land in the primary market at significant discounts. According to the company, forest land in Latvia can currently be purchased at discounts of around 40–50% compared to secondary market portfolio deals. Value creation then comes from bundling land parcels, forest management, timber revenues, and reforestation of agricultural land to generate additional carbon credits.

According to CEO Gunars, the entire FF Forest portfolio serves as collateral for investor funds. Independent valuations of the assets are expected to take place twice per year.

Looking ahead, the company plans to expand into Lithuania in March, with Finland mentioned as a later step. At the same time, FF Forest confirmed that discussions with institutional investors from Saudi Arabia are ongoing. In addition, the company received a six-figure government grant aimed at automating parts of its valuation process.

The company also expects interest rates to decline significantly in the near future. As a result, FF Forest plans to offer only around €1 million per month to retail investors, as institutional funding may allow them to refinance more cheaply.

Leave a Reply

Want to join the discussion?Feel free to contribute!